Stocks

Microcaps

Investing

Journal

Simply Better Brands

Jan 18, 2025

Over-qualified management team executing on a 3x arbitrage deal

Thoughts on a Buffett-esque arbitrage opportunity in the overlooked world of OTC Microcap stocks.

”Simply Better Brands is a rapidly growing brand accelerator in the global protein-based nutrition category, offering innovative, plant-based protein products that prioritize clean ingredients and exceptional taste.” - SBBC

It's a clearest story I've come across.

Here’s why:

Turn-around completed → boring holding company made efficient

Singular focus → Grow primary asset past 100M rev, sell it for a 3-5x multiple

Qualified team working to get paid alongside shareholders based on this singular outcome

Formerly, SBBC was a boring company holding a diverse portfolio of niche consumer packaged goods brands, ranging from cannabis to skin care. The previous management poorly allocated capital and lost focus on its best asset, TRUBAR.

Everything starts to change in early 2023 when Kingsley Ward and his PE firm, VRG Capital took interest in SBBC and purchased $7 million dollars of stock off-market securing Kingsley a seat on the Board of Directors.

About a year later in February 2024, Kingsley Ward became the CEO of SBBC. As you can see below the stock is up 207% percent since the official takeover.

In the past year, new management has:

Reduced OPEX by 36%

Replaced the board and senior management with industry veterans (E.g. Director Paul Norman who oversaw Kellogg’s acquisition of RXBAR for $600M)

Divested from almost all of the non-performing portfolio brands

Secured a $10M credit facility for the core asset TRUBAR

Positioned SBBC as shareholder friendly company, taking interviews and meetings with investors and upgraded to list on the OTCQX

Whats even more amazing, is that Kingsley and his team did this all over the course of a year!

By the way, what a monumental name… Kingsley—lots to live up to. I’m sure Malcom Gladwell could write a few words on that.

Onwards,

This brings us to TRUBAR, the core asset and MVP of Simply Better Brands.

TRUBAR is a natural, plant-based, high-protein snack primarily marketed toward women.

This focus is important because research shows that women typically make the majority of food purchases for their households (Saw a tweet on this, make of it what you will). I like this though because targeting a specific niche within a saturated market like protein bars provides a strategic edge, its bright packaging and dessert-inspired flavors are hard to miss.

I tried TRUBAR once by total chance, it was one of the healthier snack options available at a work meeting. I was very impressed with its taste considering there are no: seed oils, dairy, soy, gluten, or added sugars. It definitely checks all the boxes for the health conscious shopper.

Erica Groussman, is the founder and CEO of TRUBAR. Erica is an entrepreneur and sales expert through and through. Additionally, she is a “tru” embodiment of the brand and what it stands for. I highly recommend you listen to Erica and Kinglsy’s latest interview with Smallcap Discoveries to get to better grasp of Kingsley’s vision for SBBC, and Erica’s hands-on execution with TRUBAR.

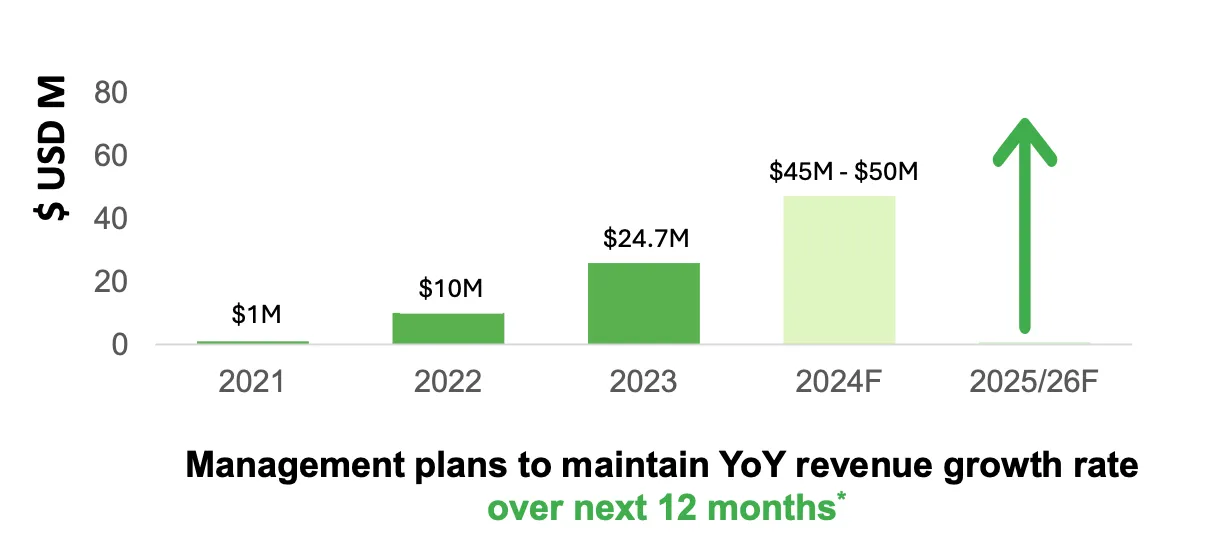

Erica has grown TRUBAR sales at 262.2% CAGR over the past 4 years.

I believe this insane growth can be attributed to Erica’s ability to get TRUBAR on to shelves across the nation. She and the team have built a huge distribution network including all the familiar favorites: Walmart, Costco, Whole Foods, CVS, GNC, and bunch more.

This past year was explosive for their retail distribution, quoted directly from their investor presentation, at the “Start of 2024 with 1500 retail locations and ended 2024 with 15,000+.”

Additionally, TRUBAR has been putting up impressive numbers online through their Amazon storefront. However, I’d discount this revenue stream since Amazon rankings are inherently less secure moats compared to physical shelf space at places like Costco and Walmart.

Looking at this history, SBBC’s goal to grow TRUBAR past 100M in sales seems totally within reason for the coming year.

So, there are many green-light attributes for TRUBAR:

Minimal debt (12.3M in current assets : 9.5M in total liabilities)

An asset-light business model leveraging co-packers and third-party vendors for production and distribution, while maintaining high 38% margins.

Theoretically, it’s a high ROCE business, but the cash won’t show up on the balance sheet since it’s being continuously reinvested into marketing spend

But forget about all of that, I believe the best way to evaluate this opportunity is not as long-term investment but as an arbitrage play.

We’re betting that SBBC, who fully own TRUBAR, will successfully execute their plan to sell the brand after hitting $100M in sales.

To put this into perspective, here’s a quote from Kingsley on the intended outcome of that story:

“We would do a special dividend for a significant portion of the proceeds from the sale of TRUBAR. Then continuing to work with SBBC to build some other brands, and we’re hopeful we can find the next TRUBAR. That's very much the plan. I’m the largest shareholder, I look forward to a special dividend of significant size in the not too distant future.” - Smallcap Discoveries Interview on YouTube

This special dividend is our arbitrage.

SBBC’s current market cap is around $84M USD. If TRUBAR reaches their sales goal, we could see a potential acquisition range in the low-end, yielding a 125% premium and in the high-end a 208% premium to today’s market cap. Here’s some rough math below:

Low-End Scenario:

A 3x rev multiple values TRUBAR at $300M.

After accounting for taxes, costs, and other factors, net proceeds could be around $210M.

Assuming 50% of that is distributed to shareholders via a special dividend, the payout would be $105M.

Premium to current market cap: ~125%

High-End Scenario:

A 5x rev multiple values TRUBAR at $500M.

After deductions, net proceeds could be $350M.

Assuming 50% distribution, the special dividend would total $175M.

Premium to current market cap: ~208%

I recently read through, Brett Gardner’s book, Buffett's Early Investments. In the chapter on Buffett’s BC Power arbitrage deal that made the partnership millions, there is an excerpt from Berkshire’s 1988 annual letter where Buffett outlines how to evaluate arbitrage situations.

This is my attempt at applying the legend’s framework to SBBC:

How likely is it that the promised event will indeed occur?

Highly Likely: TRUBAR has more than doubled sales YoY for the past 4 years, so jumping from $45M in FY24 to $100M in FY25 is on-track with historical performance.

TRUBAR is a healthy, delicious snack in a strong, growing market (protein bars), it’s probable the CPG giants will be quick to buy the brand.

How long will your money be tied up?

18 months, I anticipate TRUBAR will successfully hit their sales target this year allowing for an acquisition in 2026 or earlier.

What chance is there that something still better will transpire - a competing takeover bid, for example?

Kingsley has mentioned engaging the top firms to aid in an auction of the brand to increase competition and sale price, possibly yielding a multiple greater than 5x

However, I see this a low to mid probability, so I won’t count on it

What will happen if the event does not take place because of anti-trust action, financing glitches, etc.?

SBBC will be stuck with an wonderful business, growing sales at triple digit CAGR

Risks

It’s hard for me to find any real red-flags for this deal. I first came across SBBC through Christian Schmidt, who wrote about it on his Substack—it’s an excellent pitch. I reached out to him on X to discuss potential downsides. We both agreed that TRUBAR is the heart and soul of SBBC, and without it, SBBC isn’t a compelling long-term hold. Ideally, Kingsley would sell SBBC as a whole, rather than just its core asset.

My biggest concern is management making a stupid acquisition in an attempt to find the next TRUBAR. That said, as Whit Huguley would put it, Kingsley and his team are ’A+ capital allocators.’ I see strong parallels between Kingsley’s actions and Dayton Judd’s remarkable turnaround at Fitlife Brands that Whit has covered extensively in his annual letters.

Concluding remarks

There is so much to say, little details to dive into, threads to pull on… But, the most important thing is to get this journal out there, as it serves as snapshot in time for my thoughts and convictions on SBBC. Learning about these companies is on-going process, ever evolving. At some-point the formal research has to stop. I’m happy this time I wrote it down so I can back test it, win-or-lose.

My goal is produce at least 24 journal entries on Microcap stocks this year, averaging 2 per month. If you’d like to keep up with me on this journey please subscribe and reach out to me on X, my handle is @source_result.